How Will Epidemic Insurance Pay COVID Related Claims? 防疫新規快篩陽即確診 居家照護怎麼賠?

加入公視會員,

按讚收藏你關注的報導

The Financial Supervisory Commission decided in April that mild cases who underwent home isolation would be able to claim settlement without requiring hospitalization, as long as there is "medical behavior." The definition of medical behavior, however, has also aroused confusion and controversy. The Ministry of Health and Welfare said it will announce new guidelines.

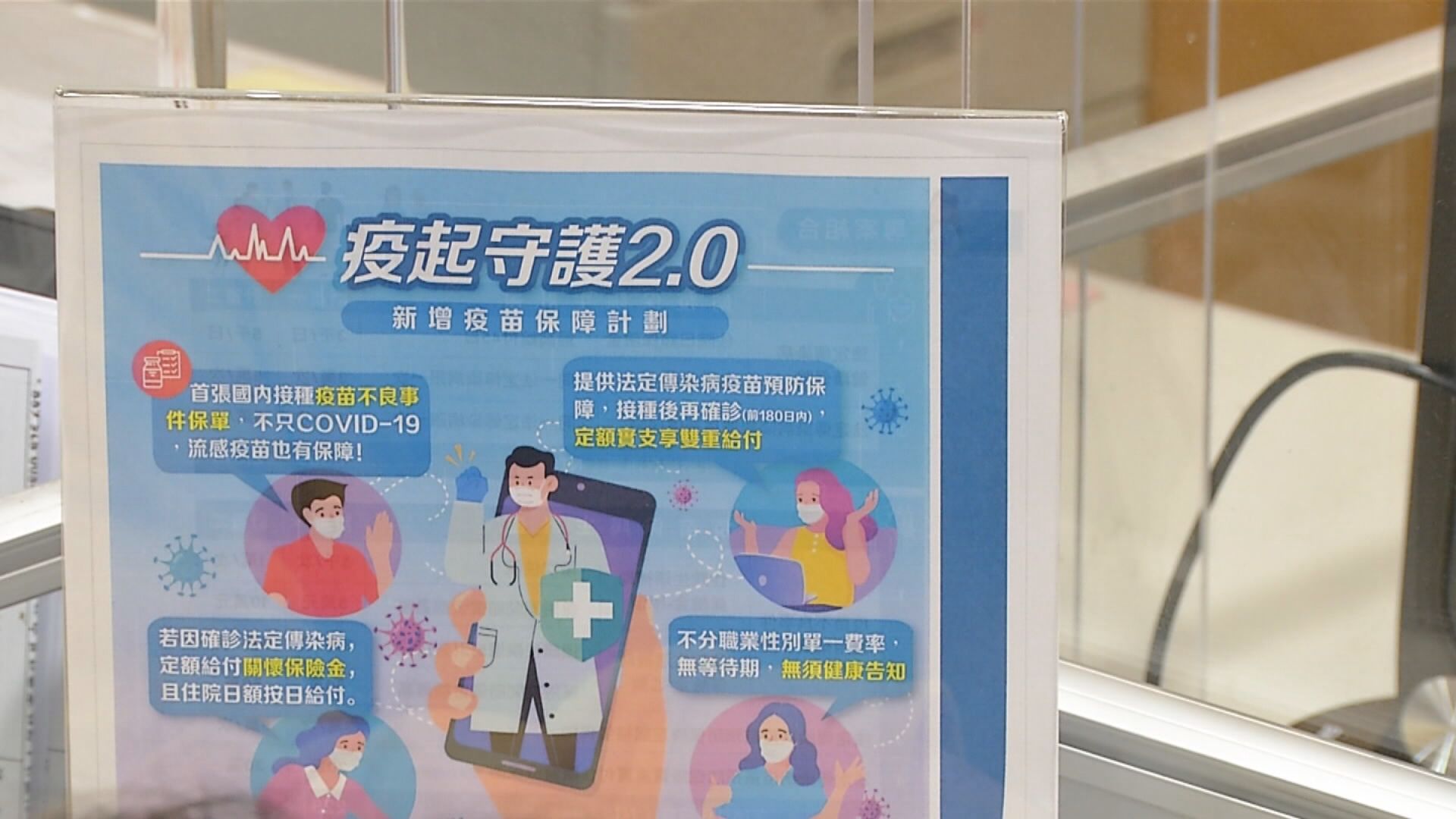

The local epidemic situation is severe, and adjustments to epidemic insurance policies have also caused controversy in the settlement of epidemic insurance claims. The Financial Supervisory Commission decided in April that mild cases who underwent home isolation would be able to claim settlement without requiring hospitalization, but only if there is "medical behavior." What kind of behaviors are required for home care to be considered medical behaviors has aroused public scrutiny.

Huang Tien-mu, Chairperson, Financial Supervisory Commission: “It depends on the final adjustment of the epidemic prevention policy by the Ministry of Health and Welfare. I think our Life Insurance Association will make some more judgments.”

Huang said that the definition of medical behavior is defined by the Ministry of Health and Welfare. FSC said it won't cross the jurisdiction lines. According to the terms of the policy, if there is no hospitalization, then it is not included in the scope of claims. However, after April 8, a large number of patients with mild symptoms were supposed to flood into hospitals. To reduce medical capacity, the FSC coordinated with the insurance industry to relax home isolation and quarantine claims. As for the behavior of home care, it is a medical behavior, which is determined by the property insurance association. In addition, a positive quick screening test will be deemed as a confirmed diagnosis going forward. Thus, the public is also concerned about whether epidemic insurance will still pay claims.

Huang Tien-mu, Chairperson, Financial Supervisory Commission: “As long as the insurance company agrees to cover this policy. In the past, if a person bought several insurance policies, the insurance companies all had this responsibility. As long as the person has a claimed accident in line with the policy's terms, the insurance companies will have to pay the claims.”

Huang emphasized that underwriting is not equal to claim settlement. As long as the insurance policy has been approved, no matter how many policies a consumer has bought, insurance companies are responsible for claim settlement. A policy's underwritten success will depend on whether the insurance company agrees to the risk. In the future, the insurance association will publish claim settlement guidelines.

本土疫情嚴峻,防疫政策的調整也讓防疫險理賠爭議不斷,由於金管會4月拍板輕症居家照護,防疫險可比照住院理賠,但前提得有醫療行為,究竟居家照護需有什麼行為才算醫療行為引發關注。

金管會主委黃天牧說:「要看衛福部最後對防疫政策的調整,我想我們(壽險)公會再去做一些判斷。」

黃天牧表示,醫療行為本來就由衛福部界定,金管會不會越俎代庖,事實上按照保單條款,要是沒有住院事實,並不包含在理賠範圍內。但由於4月8日後擔心大量的輕症者湧入醫院,失去降低醫療量能的美意,才與保險業者協調,放寬居家照護也理賠,至於居家照護有什麼樣的行為才是醫療行為,由產險公會決定。另外隨著「快篩陽性視同確診」即將全面上路,也讓各界關心防疫險是否還會理賠。

黃天牧表示:「只要保險公司同意承保的這個保單,以前他買了幾張保險公司都有這個責任,只要他一旦他發生理賠事故合乎保單約定的條款,他就要去理賠。」

黃天牧強調,核保不等於理賠,只要通過承保保單,不管消費者買了幾張保單,發生事故都有責任理賠,如果還沒同意承保,看公司依風險是否同意,未來由公會公布理賠指引。